Wednesday, July 7, 2021

As part of our ongoing efforts to provide you with relevant and important market information, please find an update from Knight Frank regarding the coronavirus.

Global House Prices

Urban house prices are rising at their fastest rate since 2007 and, of the 150 cities we track, 43 are now registering annual price growth above 10%.

A combination of powerful forces are driving house price growth; a severe undersupply of housing in many locations has been exacerbated by the slowdown in construction during the pandemic and significant numbers of buyers are locking in ultra-low mortgage rates while they can. Fear of missing out (FOMO) is also driving sales and with borders closed investors are looking closer to home to take advantage of rising prices, writes Kate Everett-Allen.

Governments in New Zealand, Canada, China, South Korea and Ireland have all taken steps to curb price inflation during the first half of this year to differing degrees of success. There are now signs, however, that some markets are cooling as the distortive effects of the pandemic ease. Canada has reported two straight months of moderating sales and Capital Economics reports that mortgage applications for US home purchases have fallen back to pre-Covid levels.

Delta

This morning’s international papers have a very 2020 feel to them. Sydney is in lockdown, South Korea is on the cusp and new cases of Covid-19 are on the rise across Europe.

The spread of the Delta variant means that as of yesterday daily cases in the UK had ticked back up to about 30,000, though the success of the vaccine roll out, which has largely decoupled infections and hospitalizations, means the reopening of the economy is set to continue. This morning’s Times reports that vaccinated travelers to England from amber listed countries will be exempt from requirements to quarantine as early as July 19th.

Consumers spent less time in British shops, bars and restaurants last month due to nervousness over rising infections, though the ultimate economic impact of the so-called third wave is likely to be limited. For more detail see Knight Frank’s updated House View, which provides a snapshot of the outlook for a range of real estate sectors, including residential, offices and retail.

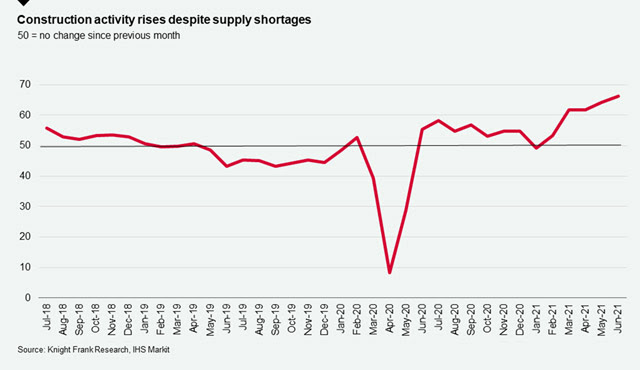

The building boom

Construction activity in June expanded at the fastest rate since records began back in 1997, according to a new purchasing managers (PMI) index from IHS Markit. The housebuilding sub-sector led those gains, after expanding at the fastest rate since November 2003.

The unprecedented surge in activity pushed both lead times and the cost of products and materials up the most since records began. Construction companies report severe shortages of stock and worsening delays in shipping and haulage, especially for products sourced from the EU. Supplies are contracting across the board, particularly for cement, concrete, plaster, steel, timber and roof tiles.

These trends are now weighing on sentiment. Though construction companies are generally optimistic about growth prospects for the next twelve months, confidence eased back to its lowest reading since January.

South Korea

Earlier this week Knight Frank talked about surging prices in global urban housing markets, led by Seoul. House prices in the South Korean capital climbed more than 25% in Q1 compared to a year earlier and local media is peppered with stories detailing the scramble for secure housing.

Much like officials in New Zealand, Canada, and China, the government is attempting to curb house price inflation and has proposed various curbs on overseas purchases of Korean homes. Official figures reveal that overseas individuals now own 21.35 million sq meters of real estate, up 78% from 11.99 million sqm in 2016, according to new analysis from Stephen Wong.

Many of those bills are still pending in the National Assembly. We expect prices to continue rising for the foreseeable future, though political desire to reign in speculative purchases is likely to prompt the introduction of new taxes with the aim of cooling activity.

In other news…

Stephen Springham on the decline of GAP and the battle for Morrisons. Plus, Will Matthews has the latest leading indicators covering inflows to equity funds, private equity activity and why the UK’s real estate sector has been growing more rapidly than previously thought.

Elsewhere – ESG outperformance looks set to end, investment industry at ‘tipping point’ as $43tn in funds commit to net zero, Lloyds Bank gets into the rental business, the quest for ‘green’ cement draws big name investors to a $300bn industry, the Pfizer vaccine and the delta variant, and finally, China bans the tallest skyscrapers due to safety concerns.

Any questions, please contact me, or the team.

{kind=link}

{kind=link}

{kind=link}